When I first encountered large purchases in business, I realized not everything is an “expense.” Some items last many years and provide value over time. Those are capital equipment.

In 2025, the global equipment finance service market alone is projected to hit $1.43 trillion, because firms around the world are investing heavily in capital assets. Understanding what is capital equipment, how it is accounted for, and why it matters can transform how you view assets and business investment.

In this guide, I will take you through a complete and up-to-date insight, including definitions, accounting rules, examples, pros and cons, and best practices in 2025. Whether you run a startup, manage operations, or study accounting, it will give you clarity on this key concept.

What Is Capital Equipment?

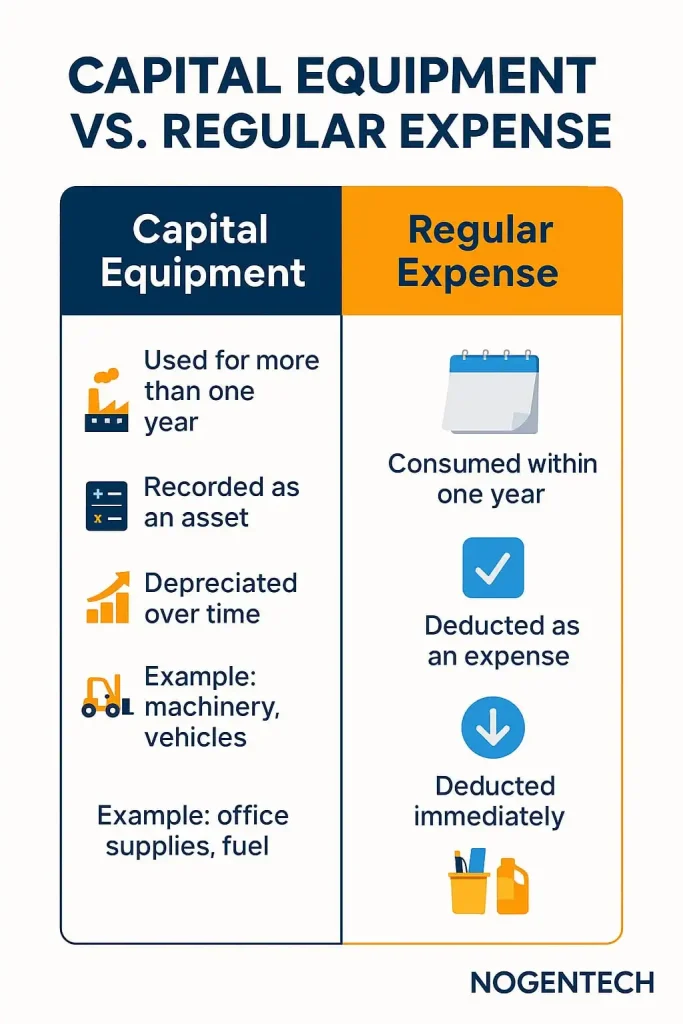

Capital equipment (also called “capital assets” or “fixed assets” in some contexts) refers to tangible, non-consumable items that an organization acquires and uses over the long term to support operations.

Such items are not used up quickly. Rather, they provide utility over multiple accounting periods. In accounting terms, capital equipment is recorded as an asset on the balance sheet and depreciated over its useful life, rather than expensed entirely in the period purchased.

A commonly used benchmark in many institutions is that a piece of equipment qualifies as “capital” if it meets both:

- A minimum cost threshold (for example, $5,000 or more)

- A useful life exceeding one year

At many universities and institutions, these thresholds and useful life criteria are clearly defined.

Because the rules can vary (by organization, by country, or by accounting standards), it is important to know your specific policy.

Capitalization Thresholds & Policies in 2025

Before declaring any equipment as capital, businesses set capitalization thresholds. It is the minimum cost and useful life for an asset to be capitalized. Items below these thresholds are expensed immediately.

- For example, many U.S. universities adopt a $5,000 threshold: any single movable item costing $5,000 or more, with a useful life of over one year, qualifies as capital equipment.

- But as of July 2025, some institutions have increased their threshold. Virginia Commonwealth University (VCU) raised theirs from $5,000 to $10,000 per item.

- Another example: Duke University’s policy, effective July 1, 2025, states that movable equipment costing $10,000 or more (or meeting their threshold) will be capitalized.

These thresholds typically include all costs required to bring the equipment into service: purchase cost, shipping, installation, taxes, and necessary adjustments.

Choosing the right threshold is a balance: too low, and you burden accounting with tracking many small assets; too high, and you may underreport significant assets. Many government accounting guidelines suggest a $5,000 baseline and encourage adjustment by asset class when necessary.

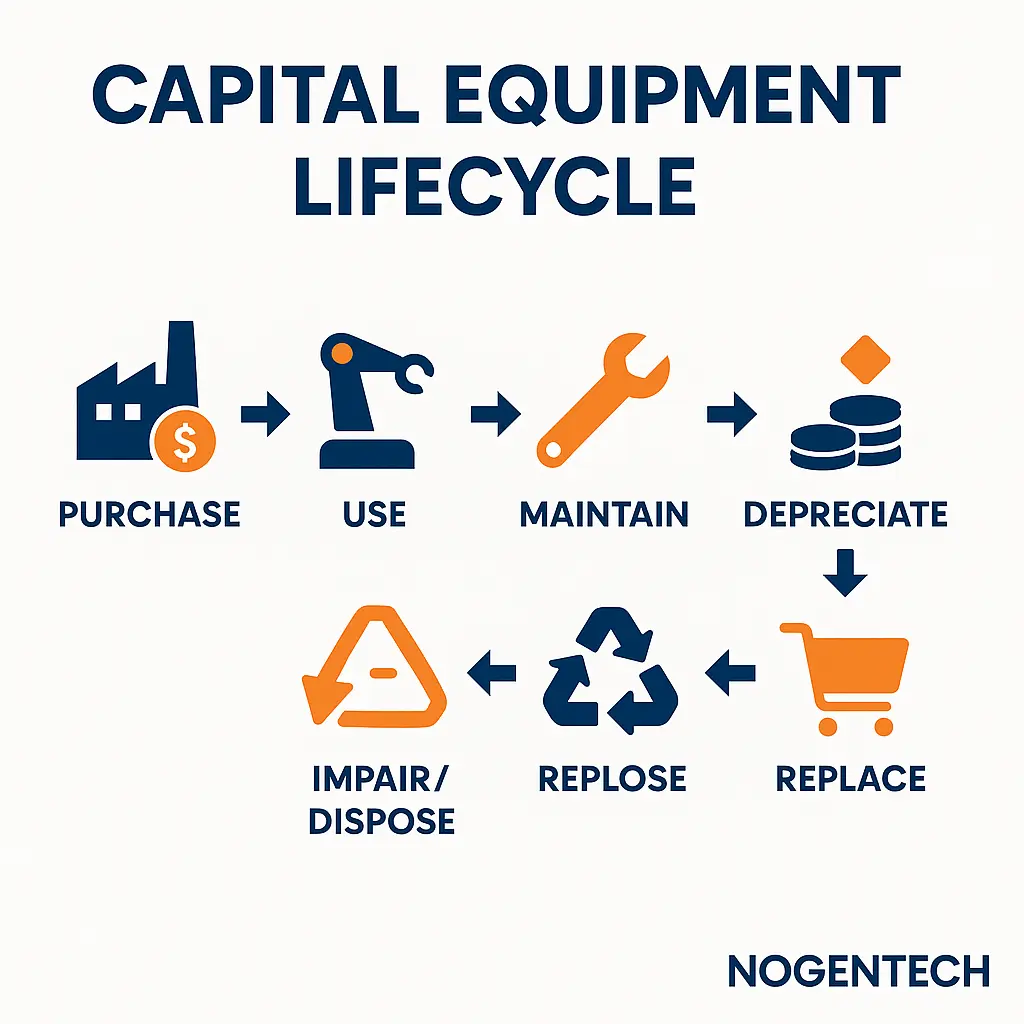

Accounting Treatment – Depreciation, Disposal & Impairment

1. Depreciation

Once classified as capital equipment, the asset is not expensed outright. Instead, you spread its cost over its estimated useful life through depreciation. The most common method is straight-line depreciation, where the same amount is taken each period. Some entities may use accelerated methods, depending on tax incentives or internal practices.

Accounting entries typically involve:

- Debit the depreciation expense over time

- Credit accumulated depreciation (a contra-asset account)

- The net book value = original cost − accumulated depreciation

Effective control over depreciation ensures your financial statements and wealth management accurately reflect asset value over time.

2. Impairment

If an asset’s value falls significantly (e.g. due to damage, technological obsolescence, or market decline), you may need to impair it, i.e. write down its book value to reflect recoverable value. This treatment ensures you don’t overstate assets on the balance sheet.

3. Disposal or Sale

When capital equipment is sold, retired, or disposed of:

- Remove the asset’s cost and accumulated depreciation from accounts.

- Recognize any gain or loss (difference between proceeds and net book value).

- Ensure proper documentation of the transaction and update asset registers.

Some organizations also perform physical inventory management and audits periodically (e.g. every 1-2 years) to confirm the existence and condition of capital equipment on record.

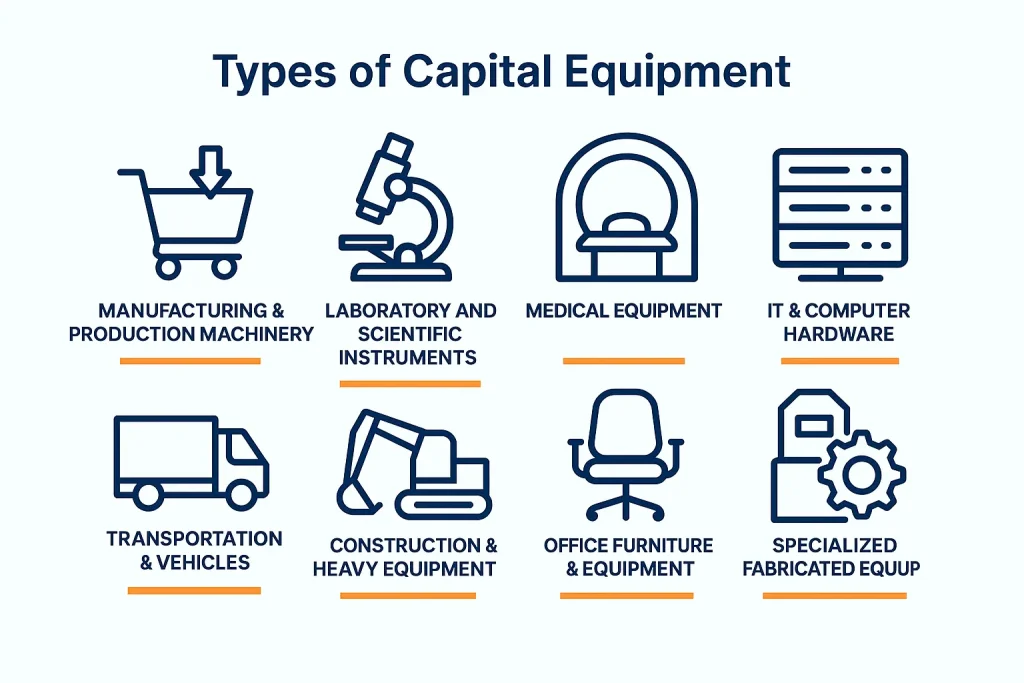

Types & Categories of Capital Equipment

Capital equipment is a broad category. Here are common types:

- Manufacturing & Production Machinery: Heavy machines in factories, CNC machines, printing presses, production lines.

- Laboratory and Scientific Instruments: Microscopes, spectrometers, diagnostic imaging equipment, testing rigs.

- Medical Equipment: MRI machines, CT scanners, dialysis machines, and surgical robots.

- IT & Computer Hardware: Servers, data centers, high-end computing clusters, networking hardware.

- Transportation & Vehicles: Trucks, company cars, forklifts, delivery vans.

- Construction & Heavy Equipment: Excavators, cranes, bulldozers, earthmovers.

- Office Furniture & Equipment: Desks, ergonomic chairs, high-capacity printers (if above threshold), conference room systems.

- Specialized Fabricated Equipment: Custom-built machinery or equipment assembled from components that collectively meet the threshold.

Examples of Capital Equipment (with Context)

Here are real-world examples (2025 context) to clarify:

- A hospital purchasing a MRI scanner for $1.5 million: capital equipment, depreciated over, say, 10–15 years.

- A research facility acquiring a high-performance computing cluster for $120,000 plus installation: capital equipment.

- A manufacturing plant installing a robotic assembly line, including robots, feeders, conveyors: capital equipment.

- A tech company installing server racks and networking hardware in its data center, provided the investment exceeds threshold.

- A construction company buying excavators or bulldozers for long-term use.

- In universities, a lab might assemble a custom piece of scientific equipment from components; if combined cost meets the threshold, it’s capitalized.

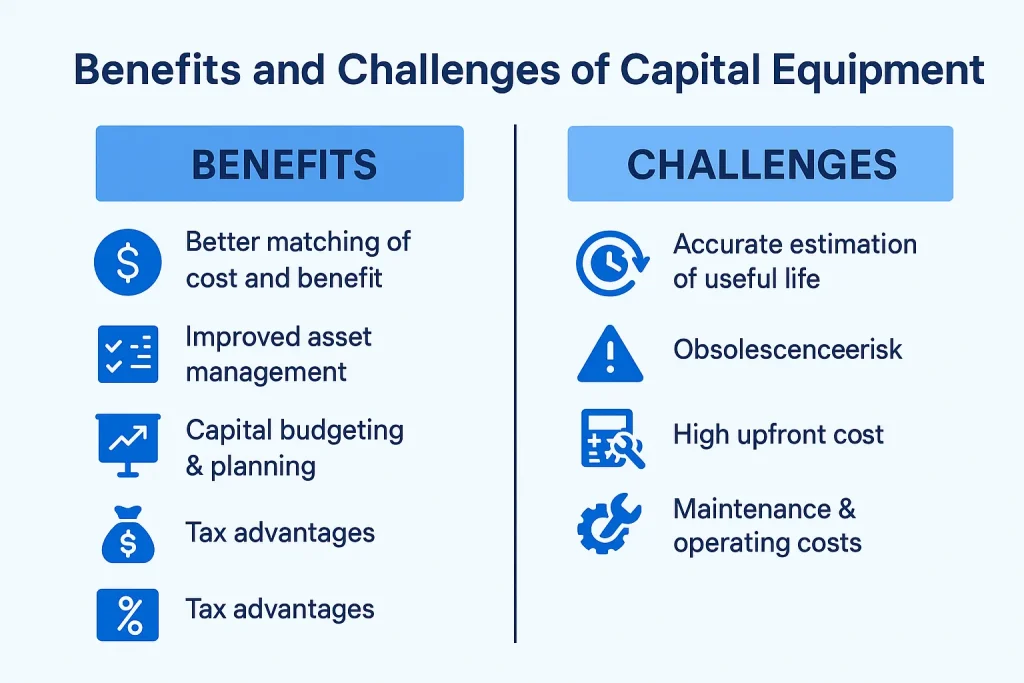

Benefits and Challenges of Capital Equipment

Benefits

- Better matching of cost and benefit: depreciation spreads cost over useful life.

- Improved asset management: tracking high-value resources.

- Capital budgeting & planning: helps in strategic investment decisions.

- Tax advantages: many jurisdictions allow depreciation deductions.

- Enhanced financial visibility: balance sheet reflects long-lived assets.

Challenges

- Accurate estimation of useful life: underestimating or overestimating can distort financials.

- Obsolescence risk: technology may become outdated before fully depreciated.

- High upfront cost: requires planning, financing, or capital allocation.

- Maintenance & operating costs: upkeep may be substantial.

- Complex accounting: tracking, impairment tests, disposal all require controls.

Best Practices for Capital Equipment in 2025

Here are practices I would recommend to organizations dealing with capital equipment:

- Set clear capitalization policies: thresholds, useful life, and asset classes.

- Include all relevant costs: shipping, installation, attachment, accessories.

- Use comprehensive asset tagging & inventory systems: barcodes, RFID, centralized databases.

- Perform regular audits: confirm assets, condition, location, usage.

- Monitor for impairment: review whether assets are still providing value.

- Plan for obsolescence: evaluate upgrades or replacement schedules.

- Train staff in accounting policies: so mistakes or inconsistencies are minimized.

- Document disposal thoroughly: record date, method, gain or loss.

- Consider bundled purchases: combining components that individually don’t meet threshold but as a whole do (if allowed).

- Review thresholds periodically: inflation or changing scale may require adjustments.

Capital Equipment and Intangible Assets

One nuance: sometimes software or intangible assets are treated like capital equipment when certain conditions are met.

For example, internal-use software development costs may be capitalized if they meet thresholds and useful life criteria. But many organizations have separate policies for software capitalization distinct from physical equipment.

Final Thoughts

Capital equipment is a foundational concept in business and accounting. It is about recognizing and managing assets that deliver value over multiple years. When you classify purchases correctly, depreciating them appropriately, and tracking them diligently, organizations gain better financial clarity and control.

In 2025, with evolving thresholds and growing technology complexity, it’s more important than ever to follow solid policies and practices. Whether you run manufacturing, research, healthcare, or IT operations, mastering capital equipment management helps ensure your investments stay productive and your finances remain accurate.

Use this guide to anchor your decisions and asset strategies.